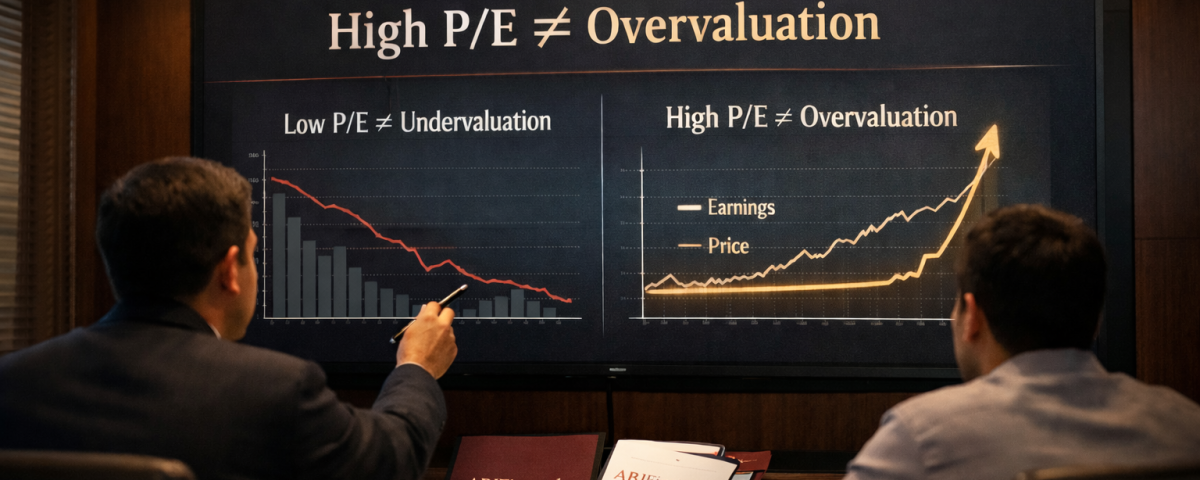

High PE ≠ Overvaluation Low PE ≠ Undervaluation

High P/E does not automatically mean overvaluation, and low P/E does not guarantee undervaluation. Understand how liquidity and market perception drive real stock prices — elements that simple ratios fail to decode.

Most investors make one critical mistake.

They look at the P/E ratio and decide instantly:

“Low P/E = Cheap.”

“High P/E = Expensive.”

What P/E Actually Tells You:

What P/E does not tell you:

It is a snapshot — not a story.

Example: The 10-Year Silent Compounder

High P/E does not mean Overpriced/Expensive

Consider a hypothetical structure:

But the stock price remains flat for 10 years, as we know its normal in stock market.

No breakout. No momentum. No excitement.

During those 10 years, intrinsic value continues compounding inside the business. Retained earnings grow. Net worth rises. Operational strength improves.

Then suddenly, the stock rallies 200%.

Now the P/E looks high.

And many investors conclude:

“Overvalued.”

But is it?

Or is the market finally recognizing 10 years of accumulated value creation?

The high P/E today may simply reflect delayed price discovery.

Real Market Equation (Short term)

Price Movement = Liquidity × Sentiment

Liquidity = Accelerator in Stock Market for stock Prices

“Without an accelerator, the car does not move.”

Fundamentals = Base foundation (Long term useful)

Let’s have an interesting example

Mostly market participants must have watched the famous series

Scam 1992: The Harshad Mehta Story.

In the series they showed how Harshad Mehta would identify fundamentally strong but underpriced companies and then aggressively build positions.

In Scam 1992, the example of Apollo Tyres is used to illustrate how price and business do not always move together. The company’s fundamentals were not created overnight — but once aggressive buying and liquidity entered the system, the stock price moved sharply in a short span. To an outside observer, the rally made prices look stretched. But the move was not about sudden business transformation; it was about market recognition and liquidity catching up.

Disclaimer:

We do not guarantee the factual of any past events referenced.

We are not attempting to judge the ethical aspects of any actions that may have influenced price movements through liquidity in the past. Market Manipulation is wrong act and going to remain wrong.

The example has been included purely to simplify and illustrate the concept for better understanding that liquidity is must to move market prices.

Where P/E Fails

Here Market repriced past growth in one shot.

Connecting above example:

After 10 years, liquidity enters: Price jumps 200%. It’s delayed pricing.

That’s real-world behavior.

Fundamental and prices don’t move hand in hand. Which P/E individually fails to decode.

Conclusion

P/E is a current snapshot, not a final judgment. A high P/E does not automatically mean overpriced, and a low P/E does not automatically mean undervaluation — both must be viewed in the context of ROCE, growth durability, earnings quality, and future visibility. Markets reprice businesses when liquidity changes. Intelligent investing requires understanding the business behind the ratios, not reacting mechanically to the ratio itself.

ABJ Finstocks Research Offerings

We provide structured investment recommendations under three categories:

{kind=link}

{kind=link}